Tuesday, February 28, 2006

Hot Caribbean Real Estate Market

American Buyers Drawn To Strong Caribbean Real Estate Market

"The Caribbean real estate market for American buyers is strong and getting stronger, according to Ricardo Cardenas, vice president and regional director of RE/MAX of the Caribbean and Central America."

"Purchasing properties in the Caribbean could be a good hedge against a domestic market that is slowing down," said Cardenas. "Property values are low in many areas, but they are appreciating rapidly, so a relatively small investment can yield good returns."

"Property values are low in many areas, but they are appreciating rapidly, so a relatively small investment can yield good returns," he added.

Here's one such bargain found along the Honduras Coast. For $490,000, you can purcahse a 5,200 square foot mansion with 300 feet of beachfront. View the details HERE.

# posted by Glen Bell @ 10:08 PM location.href=https://www.blogger.com/comment/fullpage/post/19316683/114119461541115075;>0 comments

Monday, February 27, 2006

Realty Tax Tips

CHECKLIST OF THE TEN MOST OFTEN OVERLOOKED REAL ESTATE TAX DEDUCTIONS

These are the highlights taken from a publication written by Robert Bruss and reprinted in an article in Inman News, March 3rd, 2006.

1) Home acquisition mortgage loan fees: If you bought your primary or secondary home last year, you probably obtained a mortgage to finance and purchase. That mortgage is called “acquisition mortgage” because it enabled purchase of the residence. If you paid a loan fee to obtain the acquisition mortgage, usually called “points,” that loan fee qualifies as an itemized interest deduction. Each Point equals 1% of the amount borrowed.

2) Home improvement loan fees: If you paid a loan fee to obtain a home improvement loan, that loan fee is fully deductible in the tax year it was paid.

3) Loan fees paid to refinance a home loan or borrow against other real estate: If you refinanced your existing home loan last year, or borrowed against other real estate such as an apartment building, any loan fee you paid must be deducted over the life of the mortgage; i.e., if you paid a $1,000 loan fee to refinance with a new 30-year home mortgage, you can deduct $33.33 for each of the next 30 years.

4) When refinancing, deduct any undeducted loan fees: Thanks to low mortgage interest rates, many home owners refinanced again last year after previously refinancing a year or two earlier. These home owners should remember to deduct on last year’s income tax returns any undeducted loans fees from prior mortgage refinance.

5) If you bought or sold property last year, remember to deduct prorated real estate taxes: A major tax deduction many real estate buyers and sellers overlook is the prorated property tax they paid at the close of the escrow. Even if the other party remitted the payment to the tax collector, but you were charged a prorated portion of the tax bill, be sure to deduct your share on your last year’s return.

6) Deduct prorated mortgage interest in the year of property purchase or sale: Similarly, if you bought a residence (or other real estate) and took over an existing mortgage, don’t forget to deduct your prorated interest share for the month of the sale ( even if the seller makes the payment to the lender). Your closing settlement shows your prorated share of mortgage interest.

7) Mortgage prepayment penalty: If you paid off an existing mortgage early and were charged a prepayment penalty by the lender, that prepayment qualified as an itemized deduction.

8) When land rent payments qualify as interest deductions: Millions of homes are located on leased land an Internal Revenue Code 163(c) allows land rent to be deducted like interest when the lease: (a) is for at least 15 years, including renewal periods; (b) is freely assignable; (c) contains a present or future option to buy the land; and (d) is like a security interest, such as a mortgage. Of course payments to buy the land are not deductible, nor are ground rent payments deductible if you do not have the option to buy the land, such as in a mobile home park.

9) Home construction loan interest: If you built a new home last year, or are building one now, don’t forget to deduct the construction loan interest paid. It’s deductible if the construction period does not exceed 24 months before occupancy of your principle residence.

10) Deduct prepaid property taxes and mortgage interest: If you prepaid this year’s real estate taxes last year, as home owners do to increase their tax deductions, or if you paid your January of this year mortgage payment in December of last year, don’t forget to deduct these extra mortgage interest and property tax payments on last year’s income tax returns.

**For a more comprehensive understanding of the legal/tax consequences, we strongly suggest your contacting an attorney and/or CPA for specific advice on the matters stated herein.

Compliments of Lorrie Williams and Gabriela Frey, Financial Title located in Albany, California. Lorrie can be reached at; lawilliams@financialtitle.com.

These are the highlights taken from a publication written by Robert Bruss and reprinted in an article in Inman News, March 3rd, 2006.

1) Home acquisition mortgage loan fees: If you bought your primary or secondary home last year, you probably obtained a mortgage to finance and purchase. That mortgage is called “acquisition mortgage” because it enabled purchase of the residence. If you paid a loan fee to obtain the acquisition mortgage, usually called “points,” that loan fee qualifies as an itemized interest deduction. Each Point equals 1% of the amount borrowed.

2) Home improvement loan fees: If you paid a loan fee to obtain a home improvement loan, that loan fee is fully deductible in the tax year it was paid.

3) Loan fees paid to refinance a home loan or borrow against other real estate: If you refinanced your existing home loan last year, or borrowed against other real estate such as an apartment building, any loan fee you paid must be deducted over the life of the mortgage; i.e., if you paid a $1,000 loan fee to refinance with a new 30-year home mortgage, you can deduct $33.33 for each of the next 30 years.

4) When refinancing, deduct any undeducted loan fees: Thanks to low mortgage interest rates, many home owners refinanced again last year after previously refinancing a year or two earlier. These home owners should remember to deduct on last year’s income tax returns any undeducted loans fees from prior mortgage refinance.

5) If you bought or sold property last year, remember to deduct prorated real estate taxes: A major tax deduction many real estate buyers and sellers overlook is the prorated property tax they paid at the close of the escrow. Even if the other party remitted the payment to the tax collector, but you were charged a prorated portion of the tax bill, be sure to deduct your share on your last year’s return.

6) Deduct prorated mortgage interest in the year of property purchase or sale: Similarly, if you bought a residence (or other real estate) and took over an existing mortgage, don’t forget to deduct your prorated interest share for the month of the sale ( even if the seller makes the payment to the lender). Your closing settlement shows your prorated share of mortgage interest.

7) Mortgage prepayment penalty: If you paid off an existing mortgage early and were charged a prepayment penalty by the lender, that prepayment qualified as an itemized deduction.

8) When land rent payments qualify as interest deductions: Millions of homes are located on leased land an Internal Revenue Code 163(c) allows land rent to be deducted like interest when the lease: (a) is for at least 15 years, including renewal periods; (b) is freely assignable; (c) contains a present or future option to buy the land; and (d) is like a security interest, such as a mortgage. Of course payments to buy the land are not deductible, nor are ground rent payments deductible if you do not have the option to buy the land, such as in a mobile home park.

9) Home construction loan interest: If you built a new home last year, or are building one now, don’t forget to deduct the construction loan interest paid. It’s deductible if the construction period does not exceed 24 months before occupancy of your principle residence.

10) Deduct prepaid property taxes and mortgage interest: If you prepaid this year’s real estate taxes last year, as home owners do to increase their tax deductions, or if you paid your January of this year mortgage payment in December of last year, don’t forget to deduct these extra mortgage interest and property tax payments on last year’s income tax returns.

**For a more comprehensive understanding of the legal/tax consequences, we strongly suggest your contacting an attorney and/or CPA for specific advice on the matters stated herein.

Compliments of Lorrie Williams and Gabriela Frey, Financial Title located in Albany, California. Lorrie can be reached at; lawilliams@financialtitle.com.

# posted by Glen Bell @ 6:56 PM location.href=https://www.blogger.com/comment/fullpage/post/19316683/114109604123704462;>0 comments

Monday, February 20, 2006

Housing - Just Cool or Going Cold?

Here's an article from yesterday's Sunday's San Francisco Chronicle that asks some very good questions about the real estate market. These questions are then addressed by examining past historical cycles within the Bay Area.

It's entitled; "Housing -- just cool or going cold? With home sales continuing to drop, questions about its cyclic nature are taking on a new sense of urgency." The article is written by Kelly Zito, a Chronicle Staff Writer.

Here are a few interesting exerpts to give you a flavor of the article. It's definitely well worth reading.

"The Bay Area real estate market typically runs in cycles, forming almost a stair step pattern of multiyear price increases followed by periods of stagnation or even mild declines."

"At the end of the last two major housing booms in the early 1980s and 1990s, prices in most areas did not collapse."

"On the coasts, you see price run-ups, and then instead of having large price declines, you have mild declines and flattening for a period -- it's what you'd call a stylized fact of the industry," said Andrew Leventis, economist at the Office of Federal Housing Enterprise Oversight, the overseer of mortgage titans Fannie Mae and Freddie Mac.

"Nothing leads to big declines in house prices except job destruction," said John Krainer, economist at the Federal Reserve Bank of San Francisco.

"San Francisco may have more of a chance to not have a severe (correction) because it's so hard to build here," said UC Berkeley's Rosen. "The difficulty in putting on new supply protects home prices from big adjustments."

"People ask why are home prices so high in California, and my response is: 'Everybody in the world wants to live in California,' " said Michael Carney, real estate professor at California State Polytechnic University at Pomona.

It's entitled; "Housing -- just cool or going cold? With home sales continuing to drop, questions about its cyclic nature are taking on a new sense of urgency." The article is written by Kelly Zito, a Chronicle Staff Writer.

Here are a few interesting exerpts to give you a flavor of the article. It's definitely well worth reading.

"The Bay Area real estate market typically runs in cycles, forming almost a stair step pattern of multiyear price increases followed by periods of stagnation or even mild declines."

"At the end of the last two major housing booms in the early 1980s and 1990s, prices in most areas did not collapse."

"On the coasts, you see price run-ups, and then instead of having large price declines, you have mild declines and flattening for a period -- it's what you'd call a stylized fact of the industry," said Andrew Leventis, economist at the Office of Federal Housing Enterprise Oversight, the overseer of mortgage titans Fannie Mae and Freddie Mac.

"Nothing leads to big declines in house prices except job destruction," said John Krainer, economist at the Federal Reserve Bank of San Francisco.

"San Francisco may have more of a chance to not have a severe (correction) because it's so hard to build here," said UC Berkeley's Rosen. "The difficulty in putting on new supply protects home prices from big adjustments."

"People ask why are home prices so high in California, and my response is: 'Everybody in the world wants to live in California,' " said Michael Carney, real estate professor at California State Polytechnic University at Pomona.

# posted by Glen Bell @ 10:23 AM location.href=https://www.blogger.com/comment/fullpage/post/19316683/114046096405614960;>0 comments

Friday, February 17, 2006

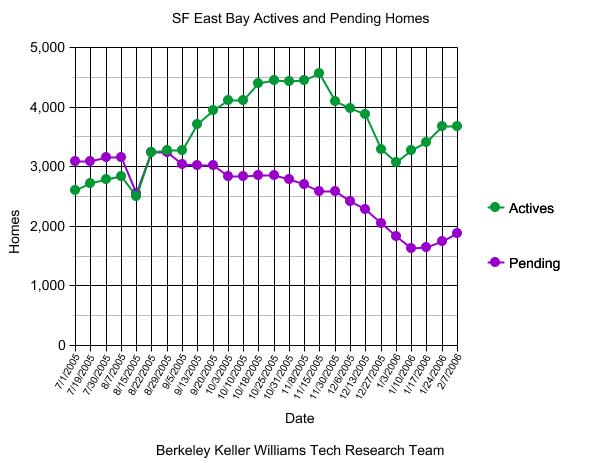

East Bay Real Estate Market Trends & Conditions

As a homeowner or real estate investor, you have probably been following the recent news reports on a cooling, or a the possibility of a bubble bursting in our real estate market? The headlines catch our attention. It’s there, in our face, almost daily, someone’s interpretation, based on some numbers, telling us of what’s really going on in our real estate markets.

One such example is a Contra Costa Times article entitled “Real Estate Market Continues to Cool,” by James Temple, based on just released statistics off of the DataQuick Information Systems site. For those who are not familiar with DataQuick, it’s one of the most up to date and more reliable research sites on real estate.

Whose crystal ball do we use? Sellers market, buyers market, normal market, housing bubble, soft landing? The information on these articles is almost always based on someone’s interpretation of old data. "Timing is everything when buying a home," is another recent article to take a look at, also written by James Temple of the Contra Costa Times.

In his article, he asks the question "is now the time to buy an East Bay home?"

"Some industry observers answer with a resounding yes or no, having deciphered clear signs from their crystal balls that housing prices will absolutely rise -- or unquestionably fall -- over the next few years. Others, however, say that timing the market is a fool's game, that personal circumstances should outweigh short-term trends and that buyers should take precautions for any eventuality."

Often times we are listening to an analysis of a market that’s anywhere from 20 to 45 days old. Furthermore, the numbers used are very general and always cover very broad areas, with the smallest statistics being based on entire cities. What most of us really want to ask, is, “what’s happening today, in our own unique neighborhoods?”

We, as real estate agents, have access to the MLS, and are able to extract up to the minute information to give us a better clue as to what’s really happening in your neighborhoods.

However, these bits of information that we are able to pull are only snapshots. Tracking these numbers over time gives us the ability to spot trends. These trends may be subject to our interpretation, but they do give us an up to date insight on a market so that we are able to make a more well informed real estate decision.

How many homes are for sale in your neighborhood, how long have they been on the market, and how many buyers are looking? (Simply put supply and demand). This translates to actives, average days on the market (actives only), and pending sales. The relationship that we find to each other in our respective markets can give us some indication as to whether we are in a sellers, a normal, or even a buyers market. This can be done on a more local basis, being able to look at your neighborhood by itself.

The past seven years we’ve had far too many buyers’ looking at a much smaller number of homes for sale. It’s been a strong sellers market every where. As stated in the article, Ken Rosen, from UC Berkeley, is quoted as saying, “There’s no question that we have moved from a seller’s market to equilibrium or even a buyer’s market in certain cases.” I have to agree with Mr. Rosen. However, this change did not happen overnight as some other news article headlines may have suggested, but gradually over the last 6 months.

The chart above tracks the number of actives (homes for sale) and the number of pendings, (homes that are in contract with buyers). The sample was taken from 34 cities within Alameda and Contra Costa Counties. Pendings have dropped noticeably in comparison to actives since July of last year. There are more homes on the market with fewer buyers. This has been a gradual change over a six month period.

Some of what you see is seasonal, some unique to this market.

The graph above measures a very large area. A sample this large, translates to being able to make only very broad general conclusions about this market overall. It doesn’t necessarily tell the story of the market in your particular neighborhood.

In reality, there are markets within markets, different neighborhoods within cities. Not every neighborhood in Berkeley, for example, will be quite the same. Some neighborhoods will have stronger markets than others. The right house, presented well, in the right neighborhood, and at the right price continues to bring multiple offers. However, in most cases, homes are staying on the market longer, and we’re starting to see some price reductions. There are also markets within price ranges. Homes that sell for under $800,000 may have a stronger market in general than homes selling for over $1,000,000.

What can you make of all this? Making your real estate decisions should be based on up to date information that reflects the conditions of your specific neighborhood. Ask your well informed real estate agent to talk to you about the market trends and conditions of your neighborhood before making that all important decision to buy or sell a home.

# posted by Glen Bell @ 11:19 AM location.href=https://www.blogger.com/comment/fullpage/post/19316683/114020401909530260;>0 comments

Wednesday, February 08, 2006

Adverse Possession – Modern Day Land Grab for Squatters?

I keep attending real estate classes where the concept of “Adverse Possession” comes up. The idea of a land grab always comes to mind with some of the newer agents. We all have this image in our mind of squatters from the old western movies putting up stakes on the open range to claim the land as their own through possession. It’s a similar idea, an idea that you rarely hear about these days. In fact, everyone that I have ever talked with knows of no one who has ever successfully attained property through this method, with but one exception, myself.

First of all; “What is Adverse Possession?” The classic definition of adverse possession is; “A method of acquiring title to real property through possession of the property for a statutory period under certain conditions by a person other than the owner of record.” For an example using a legal precedent, view the article entitled; “The Nuts and Bolts of Adverse Possession," written by Christopher Schwindt.

There are five essential elements to this process;

1) Open and notorious occupation. It does not require residency on the property.

2) Continuous for five consecutive years.

3) Hostile to the interest of the true owner and without any degree of permission.

4) Held under a claim of right or color of title. Claim of right – Adverse possessor treats the property as his own because he feels that he is the owner of the title. I have a right to this property! Color of title – Adverse possessor holds document appearing to give good title, such as a forged deed, invalid will, etc, but it does not.

5) Payment of taxes for five consecutive years.

My grandmother purchased two lots in the Oakland Hills with her brother back in the 1930’s. The property was off of Skyline Blvd with beautiful views. Their dream was to one time build and live up in “the hills.” They even placed a small RV on the land where one of her sons stayed and lived for a brief period.

“Uncle Joe” owned the property after my grandmother passed away. He had lived in New York all of his life. The Bay Area, for him, was only a place to visit on occasion and, on one such occasion, he decided to “sell” his property real cheap to his nephew’s four boys, (myself and my brothers). So we bought the two lots for what he and my grandmother had originally paid. This amounted to a couple of thousand dollars. This was back in the late 1960’s. It was "Uncle Joe's" way of leaving us, “the kids” something.

We immediately had it surveyed so that we could see what exactly we had “inherited.” We’d drive by on occasion to see what if anything was going on in the area, to walk the land and, finally sit at the property's edge to look at the panoramic views of the bay. There were no sewer hook-ups, no water and no electricity in the area at that time. The idea of building one day, once the utility services were in, was an appealing dream. We continued to pay the property taxes as had my grandmother and “Uncle Joe” had done since the 1930’s, but, as time went by, we made fewer and fewer trips to the property.

It wasn’t until years later when we put the property up for sale that we discovered there was a “cloud on title.” The property had been purchased from a Delaware Corporation, which we soon discovered was defunct.

There was only one deed that we could find, describing only one lot. In order for us to clear this up, we approached Richard Waxman, our attorney. Rick, now one of the managing partners of Wendell Rosen in Oakland, talked to us about taking a quiet title action. This is a court action brought to establish title and to remove a cloud on the title.

We were given the above guidelines. The property was again surveyed. A fence went up in the front of the property with a sign posted for the “world” to see our claim of ownership. We spoke with neighbors to see if any claim other than ours was even a remote possibility, and found nothing.

Finally after a five year period, we felt that we had established through “adverse possession,” ownership of the property. The case went to court and although it was an unusual procedure, even for the judge, (her first such case), it was made so very obvious to her that there were no other claims to this property but ours. The court awarded us title and the property was eventually sold.

This is such a rare procedure. Again, I have heard of no one, other than ourselves, ever having successfully claimed property in this manner. What we had in our favor was the truth, that the property was indeed ours. Adverse Possession was only a means to clearing title.

The point of the story is that such a thing can happen. It is possible. The intentions of the law were to protect people like us, however, it does open up the possibility of land being taken without your knowledge if you are not careful. Leaving land that you own alone for long periods of time without improvements could run the risk of loss by such a quirky law. So, just in case, for those of you with concerns of ever having this remote possibility ever happen to you, I’ve included an article for you to take a look at as a precaution, “Understanding – and Avoiding – Adverse Possession" written by Benny. Kass.

First of all; “What is Adverse Possession?” The classic definition of adverse possession is; “A method of acquiring title to real property through possession of the property for a statutory period under certain conditions by a person other than the owner of record.” For an example using a legal precedent, view the article entitled; “The Nuts and Bolts of Adverse Possession," written by Christopher Schwindt.

There are five essential elements to this process;

1) Open and notorious occupation. It does not require residency on the property.

2) Continuous for five consecutive years.

3) Hostile to the interest of the true owner and without any degree of permission.

4) Held under a claim of right or color of title. Claim of right – Adverse possessor treats the property as his own because he feels that he is the owner of the title. I have a right to this property! Color of title – Adverse possessor holds document appearing to give good title, such as a forged deed, invalid will, etc, but it does not.

5) Payment of taxes for five consecutive years.

My grandmother purchased two lots in the Oakland Hills with her brother back in the 1930’s. The property was off of Skyline Blvd with beautiful views. Their dream was to one time build and live up in “the hills.” They even placed a small RV on the land where one of her sons stayed and lived for a brief period.

“Uncle Joe” owned the property after my grandmother passed away. He had lived in New York all of his life. The Bay Area, for him, was only a place to visit on occasion and, on one such occasion, he decided to “sell” his property real cheap to his nephew’s four boys, (myself and my brothers). So we bought the two lots for what he and my grandmother had originally paid. This amounted to a couple of thousand dollars. This was back in the late 1960’s. It was "Uncle Joe's" way of leaving us, “the kids” something.

We immediately had it surveyed so that we could see what exactly we had “inherited.” We’d drive by on occasion to see what if anything was going on in the area, to walk the land and, finally sit at the property's edge to look at the panoramic views of the bay. There were no sewer hook-ups, no water and no electricity in the area at that time. The idea of building one day, once the utility services were in, was an appealing dream. We continued to pay the property taxes as had my grandmother and “Uncle Joe” had done since the 1930’s, but, as time went by, we made fewer and fewer trips to the property.

It wasn’t until years later when we put the property up for sale that we discovered there was a “cloud on title.” The property had been purchased from a Delaware Corporation, which we soon discovered was defunct.

There was only one deed that we could find, describing only one lot. In order for us to clear this up, we approached Richard Waxman, our attorney. Rick, now one of the managing partners of Wendell Rosen in Oakland, talked to us about taking a quiet title action. This is a court action brought to establish title and to remove a cloud on the title.

We were given the above guidelines. The property was again surveyed. A fence went up in the front of the property with a sign posted for the “world” to see our claim of ownership. We spoke with neighbors to see if any claim other than ours was even a remote possibility, and found nothing.

Finally after a five year period, we felt that we had established through “adverse possession,” ownership of the property. The case went to court and although it was an unusual procedure, even for the judge, (her first such case), it was made so very obvious to her that there were no other claims to this property but ours. The court awarded us title and the property was eventually sold.

This is such a rare procedure. Again, I have heard of no one, other than ourselves, ever having successfully claimed property in this manner. What we had in our favor was the truth, that the property was indeed ours. Adverse Possession was only a means to clearing title.

The point of the story is that such a thing can happen. It is possible. The intentions of the law were to protect people like us, however, it does open up the possibility of land being taken without your knowledge if you are not careful. Leaving land that you own alone for long periods of time without improvements could run the risk of loss by such a quirky law. So, just in case, for those of you with concerns of ever having this remote possibility ever happen to you, I’ve included an article for you to take a look at as a precaution, “Understanding – and Avoiding – Adverse Possession" written by Benny. Kass.

# posted by Glen Bell @ 6:04 PM location.href=https://www.blogger.com/comment/fullpage/post/19316683/113945160909834711;>0 comments

![]()

Links

Links

{kind=link}