Sunday, November 04, 2007

Overpricing House May Boomerang on the Seller

If you're thinking of putting your house on the market soon, then I think you'll be interested in taking a look at this article by Kathleen Lynn. Read the entire article HERE.

"Realtors often warn sellers about the danger of overpricing a house. Now they have evidence to show skeptical clients: research by Jeffrey Otteau, a New Jersey appraiser."

"He found that in a market where prices are declining, sellers who "test the market" with a high price usually end up with a lower price than those who price realistically."

Otteau, of Otteau Valuation Group, studied about 4,500 home sales that took place in the first half of 2007.

"He looked at houses that sold in less than a month, and found that they had a median asking price of $599,900 and sold for almost full price - a median of $599,000. When he looked at houses that lingered on the market for more than a month, however, he found that they were priced higher - at a median of $634,900 - but actually sold for less, a median of $585,000. The median is the point at which half the sale prices are above and half below.

"With a high price, the house stays on the market as buyers ignore it in favor of lowered-priced competitors. In an environment of falling prices, a house that sells three months from now is going to command a lower price than one that sells today."

"Houses that are priced right are selling," said Otteau. "Overpricing extends days on the market and guarantees that you will sell your home for less in a declining market."

"Otteau said pricing a house a little below the competition not only catches the buyer's interest - it also reassures them that they won't kick themselves later for overpaying if, as expected, home prices drift lower in 2008."

"Agents should aim to underprice the competition."

"You can't just try for a higher price because you really want it," he said. "The way to get a higher price is to create a sense of urgency by setting a lower price."

Labels: Bay Area Real Estate, Housing Market, Median Home Price

Monday, October 08, 2007

Watching for Signs of a Market Turnaround

Her conclusion; "There are good buying opportunities in the current market for well-qualified buyers. Just make sure that you pick your bargains carefully." Read her entire article HERE.

Lew Sichelman, United Media Feature, speaks about how most would-be buyers have taken themselves out of the market until prices "hit bottom."

That could be a mistake for those who plan to stay in their new home for quite awhile. "The common wisdom is that if the house of your dreams comes along, go for it. After all, it may not be available six months from now. As long as you remain in the house, any further drop in prices will be offset by rising prices down the road."

If you look at home prices over the past 40 years, there is a very predictable cycle: Home prices increase for several years, are followed by a slight price drop and then stay flat for the next few years. You can see this pattern on a graph. Although they vary somewhat by location, they usually follow the same pattern.

Lew Sichelman states; It's tough to know the precise moment when prices stop falling and start rising once again. It's not even easy to spot a trend reversal. "If it was so easy to find the bottom," Markstein,(a senior economist with the NAHB), said, "we'd all be millionaires."

He goes on to say that "there are telltale signs that smart buyers can look for, evidence that the housing market has finally firmed and is about to rebound."

His key vital signs include;

Existing Home Sales

Building Permits

Mortgage Defaults

Foreclosure Sales

Mortgage Rates

You can read in detail about his five keys to look for HERE.

There are a few sources that can help your with you research. Your knowledgible realtor of course. DataQuick has some of the most up to date news and statisitics on housing markets. CAR, California Association of Realtors, is another good resource. Inman News always has good articles on Real Estate. On a national basis, you can visit NAR, the National Association of Realtors.

Labels: Bay Area Real Estate, CAR, DataQuick, Housing Market, Inman News, NAR, Real Estate Cycles

Friday, August 17, 2007

Buyer's Opportunity?

Have prices hit bottom, or do they have further to go? How long will the housing recession last?

These real estate cycles typically last from two to five years. Most forcasters are pointing towards this winter to be the valley or low point of this down cycle with some relief coming sometime in 2008 or as late as 2009 depending on which source you listen to.

Lawrence Yun, NAR senior economist, said he isn’t looking for any notable changes in sales activity. "Mortgage disruptions will hold back sales over the short term, but long-term fundamentals are favorable. A modest upturn is projected for existing-home sales toward the end of the year, with broader improvement to include the new-home market by the middle of 2008."

"More buyers, and cutbacks in new construction, will eventually draw down the inventory levels and support future price appreciation, but general gains will be modest next year. Serious buyers today have a long-term view of housing as an investment – speculators have left the market."

View the U S Economic Outlook - August, 2007, from NAR, HERE.

"This isn't going to get better until this unsold inventory gets absorbed," said Standard Pacific's Delva, "And this isn't going to happen until the financing issues are resolved; the smart money has the slump ending in the latter half of next year or some time in 2009." Story by Robert Hollis, San Francisco Chronicle. View the full story Here.

Delva and other builders say a key turning point will be when potential buyers return to the market, convinced that the value of what they're buying won't continue to decline.

When that happens, "There's going to be a slew of buyers coming out of the woodwork," said KB Home's Burnstein.

Will this winter be one of the best buying opportunities that we've seen in years?

Interest rates, although much harder to obtain, are still at their lowest levels in decades. Rates on 30 year mortgages sank last week to their lowest point in two months, a dose of good news for people thinking about buying a home. "30-year rates lowest since the end of May.

"As of last week, the market for conforming mortgages was still operating smoothly, and if you qualify for one, you shouldn't have trouble getting a mortgage at a reasonable price." - Kathleen Pender also of the Chronicle.

So far, borrowers with decent credit histories and the ability to document their income - "the majority of the home-buying public" - aren't being shut out from getting a loan. - CNN, "Six Questions Consumers Are Asking About The Mortgage Market," By Amy Hoak

"Sellers can no longer be reluctant to accept offers or reduce prices. Tightening credit and diminishing mortgage products will continue to reduce the pool of qualified buyers. This, along with the increase in national housing inventories, means now is not the time to hold out for the best price possible." - Alexandra Saunders, BGS Financial.

The median price of American homes is expected to fall this year for the first time since federal housing agencies began keeping statistics in 1950.

Should I wait or buy now?

Alexandra goes onto say; "Potential borrowers cannot wait any longer. For those who are considering buying a home, be aware that the volatile credit market can change overnight, leaving fewer options available to borrowers attempting to qualify for a mortgage. With decreases in home values and fewer available mortgage instruments, delaying any longer could get significantly more expensive."

This isn't fully realized until you weigh in the effect of waiting for prices to drop while interest rates continue to increase. So, you have to ask yourself, in the coming months, do I expect interest rates to increase? If so, how much more must home prices drop to counter the effect of rising interest rates?

The buying season typically slows after the summer months with a drammatic drop-off by mid October. With so much inventory and uncertainty in the mortgage & real estate markets, there should be plenty of "bargains" this winter.

"The key theme is that while it may be a different mortgage landscape, it still can be a good market in which to buy - as long as people are buying for the right reasons and are paired with loans that ensure they will be able to keep the home in the future." - CNN

Labels: Bay Area Real Estate, CNN, Housing Inventory, Housing Market, Interest Rate, Real Estate Cycles, San Francisco Chronicle

Thursday, December 28, 2006

Selling Home in '07 Requires New Approach

"If you're going to sell next year, the key to a successful closing will be planning. To get you going, here is my annual list of home seller resolutions you might want to keep."

Ilyce Glink of Inman News gives us the following pointers in her article posted today.

1. Overcome any possible objections a buyer would have.

Sellers don't often understand that their primary job is to not only eliminate any potential objections that would stand in the way for a buyer to make an offer but to exceed their expectations as well. If your home is competitively priced, and your home's condition exceeds a buyer's expectations, you'll get the offer you want.

2. Get my home into shape before I let anyone see it.

Getting a home into "selling shape" is quite different from even having a clean, beautiful home. You need to "stage" your home, which means you have to make it look exactly the way a buyer thinks it should.

For best results, do this before you invite any real estate agents or brokers in to assess how much it is worth. The agents you interview will be your "Wow!" test. If they walk into your home and say, "Wow! What a great place you have here," you know you've done it right.

How do you stage a home? Start by throwing away, giving away or packing away anything you haven't used in the last three to five years. You should also give your home a thorough cleaning and address any small fixer-upper projects you've been putting off.

Once your home is clean, you can assess what kind of other work needs to be done. Should you give your home's interior and exterior a fresh coat of white paint? Do you need to power wash your vinyl siding? Should the windows be washed? The wood floor polished? New wallpaper put up in the guest bathroom? Does your landscaping require a visit or two by a professional landscaper? Whatever you decide to do, make sure it's completely finished before you invite anyone over to see your home.

Finally, move out excess furniture, buy matching towel sets for the bathroom, and make sure you have a new cover with matching pillows for your bedrooms. Your home should look very put together, as if you were auditioning for the cover of a home decorating magazine.

3. Invite at least three agents to create a comparative marketing analysis.

Often, sellers simply call the agent who sold them their home to list it. While you may end up with that person, you'll be doing yourself a favor if you invite a couple of other agents in from different firms.

Why? Because each agent will have a different marketing plan and idea about how much your home is worth. If you invite three agents to prepare a comparative marketing analysis (a CMA is a sales tool that analyzes homes similar to yours that have recently sold, presents a marketing plan and suggested list price), one will bring in a high price, one a low price, and one somewhere in between. Each may have a slightly different idea about how to market your home, or give you ideas that you can share with the agent you finally choose.

If you don't like any of the three agents you've invited to your home, get some referrals and invite additional agents to prepare a CMA. One good way to get agent referrals is to ask the agents you invited to do a CMA who they think is the best agent in town (other than themselves, of course).

4. Know what my selling timetable is before I list my home.

Do you want to sell or do you need to sell? If you need to be out in three months or less, you'll need an aggressive agent with a very competitive list price. If you've got six months or a year in which to sell, you may choose to price your home a little higher, or may choose a different type of agent. Knowing when you have to move -- and sharing that crucial bit of information with your agent -- allows you to choose a correct pricing and marketing strategy.

5. Be realistic about the market.

After a half-dozen years of a super-hot seller's market, the tables have turned in many markets. Expensive homes are selling more slowly than homes priced for first-time buyers. (Although homes priced at $10 million and above seem to be selling at the same pace as always.)

Accept the reality of your local market and make sure you price your home realistically. Don't blame your broker if you don't get three offers over your list price within 24 hours of putting your home on the market. Sellers who set sky-high prices could wait months for an offer and may wind up with the same price they would have had if they'd priced their home correctly the first time -- or a lot less.

6. Know where I'm going.

Once you've decided to sell, you ought to think about where you want to go. Often, people move to another home within the same general neighborhood. But if you're moving to a different city, state or part of the country, you'll need to do your homework ahead of time. Start researching neighborhoods that offer the amenities you're interested in. Don't wait until you have a contract on your home. That's the time you should be seriously looking to put in an offer on your new home, not start the process of exploring neighborhoods.

Or, if you're not sure what you want to do, consider renting on a short-term or month-to-month lease. These days, landlords are hurting and they may be perfectly happy to accept a six-month lease.

7. Read all documents thoroughly before I sign them.

Why would someone sign a legal document he or she hasn't read? I'm not sure, but home sellers do it every day. If you're going to sell (or buy) in the coming year, promise yourself that you'll take the time to read and understand the listing contract, offer to purchase, and loan documents for your next purchase. (If you're taking back a loan for the home buyer, have an attorney prepare the documents so you are sure to be protected.) Unless you've got cash to spare, a mistake in these documents and the warranties they contain could seriously affect your finances.

8. Set my minimum sales price.

Everyone wants to get his/her list price. But unless you're in a strong seller's market (where there aren't enough homes to meet the demand), it's unlikely you'll get it. That means you'll probably get an opening offer that's somewhat below your list price.

In order to negotiate effectively, it helps to determine the minimum amount you'll be happy accepting for your home -- before you put your property on the market. This is a price that will allow you to walk away happy. If you receive an offer with anything above this price, it's like gravy. If it's below the minimum price you've set, you can negotiate accordingly.

The psychological benefit of a minimum acceptable price is great: It puts you in control of an emotional situation by helping you to distance yourself emotionally from the negotiation process.

9. Not be driven by greed.

One big mistake many sellers make is to get a little greedy, particularly if the first offer is above the minimum acceptable price you've set. Then, the negotiation becomes a game of how much you can get.

Remember, a successful sale means everyone walks away feeling happy. If you get so greedy that the buyer walks away, you've let the deal get the best of you. Resolve to be reasonable and you'll end up shaking hands with the buyer at the closing.

Labels: Bay Area Real Estate, Housing Appreciation, Housing Market, Inman News, Real Estate Cycles, Staging

Wednesday, December 27, 2006

Top Ten Tips on Increasing the Value of your Home

Here are the Top Ten Tips to increase the value of your home as offered by the House Doctor, Ann Maurice. For further reference, her website can be found HERE.

1. You need to present your house so that it will appeal to the broadest possible buying audience. The trick is to ensure that they can imagine themselves living there as soon as they walk in.

2. Clear the clutter. Mess all too easily becomes familiar junk which we are used to having around. It makes rooms look smaller and sends unhelpful messages to your buyers. Tidy away family photos and books. If you can't find space to store the less personal stuff, take as much as possible to the nearest dump.

3. Elbow grease can add more value to your house than almost anything else. Clean, clean and clean some more. The kitchen and bathroom are the two most important rooms, but don't stop there. Dust every surface, ornament and lampshade you possess.

4. Make sure all entrances are uncluttered, warm and welcoming. Mark the path to your front door with potted plants on either side. Make sure the doors open properly and aren't hampered by a row of coats or muddy boots behind. Check that furniture doesn't stop any of the internal doors from opening or shutting properly.

5. Potential buyers won't be able to visualise themselves living in your home if the walls are bright, patterned or just plain ugly. Paint them in light, neutral colours. You can introduce splashes of colour with rugs, cushions, throws, table runners and flowers.

6. You can make a world of difference to a dark entrance hall with a strategically placed mirror. Carefully positioned, it will add space and maximise the available light. Ensure that it is hung at eye level.

7. Do all those little jobs round the house that you've always meant to finish. If you don't know what you're doing, get someone in who does. Broken window catches, a front door bell that doesn't work or half-finished shelves convey an air of neglect and signal to a potential buyer that there may be other, more significant aspects of the house that have been left undone.

8. Ensure that every room has a clear function and purpose. Play up the existence of a dining room by clearing away all the children's homework and games. A third bedroom could be a bedroom, a study or a dressing room, but not all three at once. Organise some storage systems so that the principal function of the room they're in remains clearly defined.

9. A carpet that is dark or heavily patterned dominates a room and makes it seem smaller. Replace carpets that are old, worn or just dirty. This may seem an unnecessary expense, but it will lift the appearance of the room and your buyers won't be imagining the extra cost of replacing the carpet themselves.

10. Be ruthless when it comes to dealing with your pets. It's easy to get used to their smell - so ask a friend to be brutally honest with you. Does your house smell? Before each viewing eliminate unpleasant smells and banish pets to a willing friend's while you are showing people round. Get rid of pet hair too - brush and vacuum until you're sure it's gone.

Labels: Ann Maurice, Bay Area Real Estate, Housing Appreciation, Housing Market, Real Estate Cycles, Staging

Tuesday, December 26, 2006

Homeowners Find Bidding Wars Over

By Rachel Konrad, AP Business Writer

"Although few experts predict that home values will fall dramatically in 2007, many economists say that prices won't improve for 12 to 18 months. And without the cushion of rising home equity -- which softened the blow of high oil prices last year and kept consumers buying big-ticket items at a rapid clip -- Americans may lose confidence in their finances, and the broader economy is likely to suffer."

"Ambitious building booms in many markets in the past half-decade, combined with mortgage interest rates that have increased about 1 percent in the past year, have resulted in residential real estate stagnation. The gridlock defies conventional wisdom, stubbornly remaining neither a buyer's nor a seller's market."

"We are currently experiencing the worst of the market freeze, which is being exacerbated by the gap between the buyer's desire for bargains and the seller's fantasy of what they once thought their homes would be worth," said Diane Swonk, chief economist for Chicago-based Mesirow Financial, who forecasts a rebound in early 2008. "The good news is that there are some signs of stabilization. The bad news is that a substantial backlog of unsold homes still exists."

"The newest forecast by Moody's Economy.com, a private research firm, projected that the median sales price for an existing home will decline in 2007 by 3.6 percent -- the first decline for an entire year in U.S. home prices since the Great Depression of the 1930s."

"Areas along the coast of the nation and the large urban areas tend to see stronger price gains in housing upturns, and stronger declines in downturns," said Celia Chen, a housing economist with Moody's Economy.com in West Chester, Pa.

"We have to work off the inventory," said Daniel Nussbaum, a licensed investment adviser and CEO of Calabasas-based TheUSARealty.com. "I honestly think we're past the worst of it, but if you don't take out your magnifying glass you might not notice."

"It's definitely a friendlier market than earlier this year, but not a dramatically cheaper one," Zach Chouteau, 41, said. "People have gotten really spoiled by the rapidly escalating prices, and it seems like they're in denial that things have leveled out. They're just fishing for the best price."

Labels: Bay Area Real Estate, Housing Inventory, Housing Market, Moody's Economy, Rachel Konrad, Real Estate Cycles

Saturday, November 25, 2006

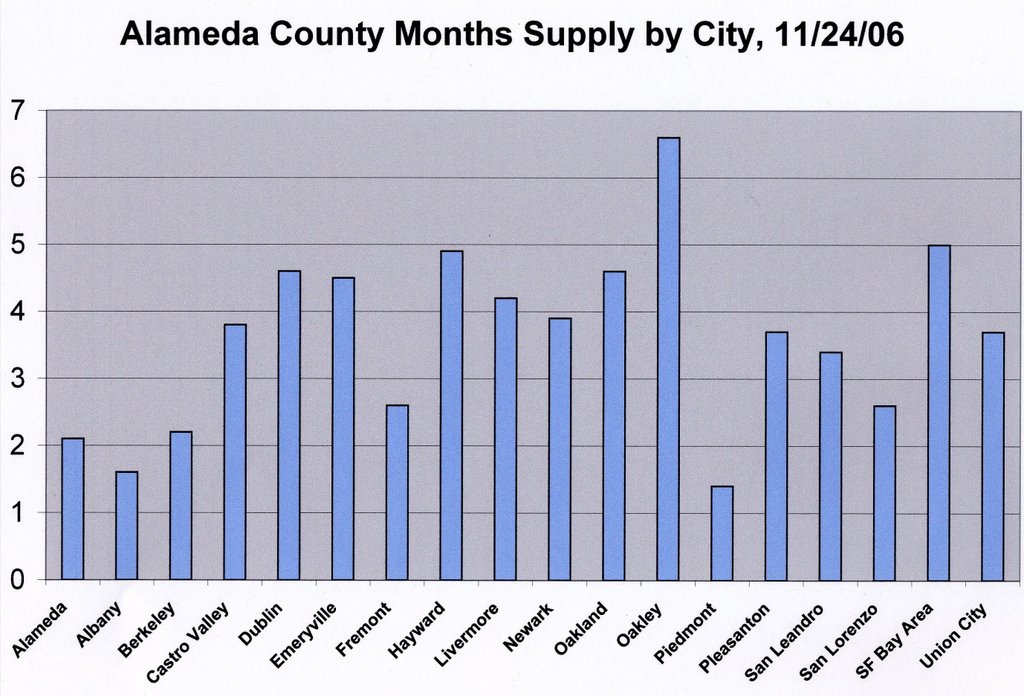

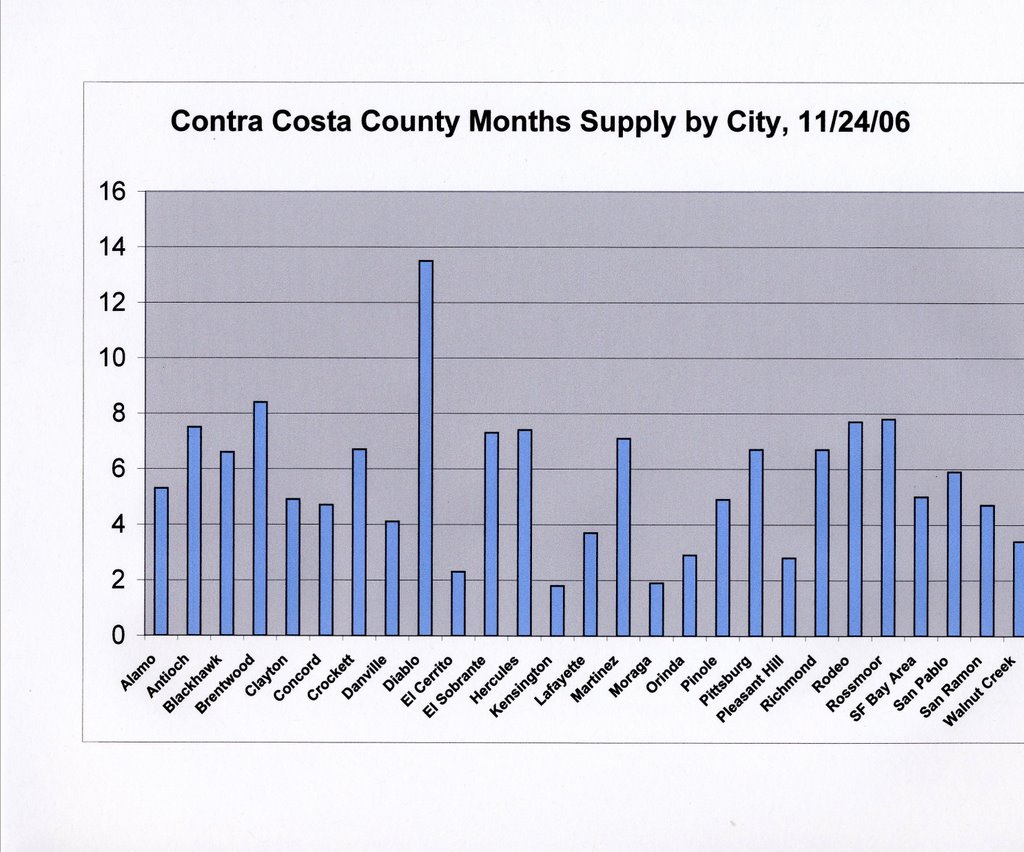

East Bay Housing Inventory Stacks Up

"As the housing market slows down, many areas in the East Bay are showing a growing inventory of homes sitting on the market. And while Antioch and Brentwood are at the top of the list of standing inventory, so are Rossmoor in Walnut Creek, Alamo and Diablo." as stated in an article in today's Contra Costa Times, written by Barbara Hernandez, and entitled "East Bay Housing Inventory Stacks Up."

Basically, the months supply is the ratio of inventory to sales. What it tells us is how many months the stock of homes for sale would last, if sales continued at their current rate. The "State of Equilibrium" is considered to be 6 months and the norm for housing inventory. This is the state where there considered to be an equal number of sellers and buyers. This can also be used as a guage as to whether we are in a "Buyer's," "Normal," or "Seller's" market.

Basically, the months supply is the ratio of inventory to sales. What it tells us is how many months the stock of homes for sale would last, if sales continued at their current rate. The "State of Equilibrium" is considered to be 6 months and the norm for housing inventory. This is the state where there considered to be an equal number of sellers and buyers. This can also be used as a guage as to whether we are in a "Buyer's," "Normal," or "Seller's" market."Bay Area home sales held steady at a five-year low in October as buyers and sellers circled each other in a game of wait-and-see. Prices remained flat, a real estate information service reported." - DataQuick

"The year 2006 marked a turning point in the California housing market. After four successive years of new records for both statewide sales and the statewide median price, the existing home market declined sharply in 2006, while price appreciation slowed with each passing month." - 2007 Housing Market Outlook as posted in CAR, (California Association of Realtors).

A Summary of CAR's Forcast for California in 2007; "The market should see less of a decline in sales in 2007, with an anticipated 7 percent decline in statewide sales for 447,500 homes. Inventories will remain in the range of the long run average of 7 months through much of 2007. Inventories, affordability constraints, and a continued gulf between seller aspirations and buyer expectations will result in a 2 percent decline in the median to $550,000 in 2007." You can find the current NAR national forcast HERE.

Home prices fall, after 4 hot years. Median figure for Bay Area dips from $616,000 to $611,000.

"The Bay Area could be following other regions of the country that already have experienced a decline in prices. The National Association of Realtors reported that the median price for a house nationwide fell 1.7 percent to $225,00 from $229,00 in August, the first drop since 1995."

"Historically, California has had about 7 to 10 months of inventory, according to the realty group. This means the current supply is close to normal but it feels like a significant change after a tight market. As buyers continued to take their time, the number of homes sold sank to a five-year low last month, dropping almost 30 percent from September 2005, DataQuick found. The total number of houses and condos sold fell to 7,907 in September from 11,205 a year earlier." - San Francisco Chronicle, Marni Leff Kottle.

"Most homeowners are simply going to wait out the slowdown," said Leslie Appleton-Young, chief economist for the California Association of Realtors.

Labels: Bay Area Real Estate, DataQuick, Housing Inventory, Housing Market, Months Supply, Real Estate Cycles, San Francisco Chronicle

Tuesday, April 25, 2006

Staging Your Home Will Help You Sell It More Quickly and Bring a Much Higher Price

"Staging your home," East Bay Business Times" - April 21, 2006by Gina Vierra

Labels: Bay Area Real Estate, East Bay Business Times, Housing Market, Staging

Monday, April 24, 2006

Mortgage Lenders: Who's Most At Risk

"As delinquency rates rise, red flags are flying over some aggressive finance outfits," as stated by Mara Der Hovanesian, of BusinessWeek.

"For months doomsayers have been predicting that the slowing housing market, along with rising interest rates, would lead to mortgage foreclosures and bank losses. That hasn't happened yet, but delinquency rates have started to rise. What's worse, instead of cutting back on the exotic mortgages they've leaned on throughout the boom, many lenders are charging ahead on such high-risk loans full tilt. "Mortgage lending standards show little sign of tightening," says Frederick Cannon, bank analyst with New York's Keefe Bruyette & Woods Inc. investment bank. "[Lenders] should have dialed back the aggressive loans by now."

"The much-feared troubles may finally be arriving. Delinquency rates jumped more than 7%, to 4.7% in the fourth quarter of 2005, from the year before, according to the Mortgage Bankers Assn. Home buyers are becoming over-extended. In California, where seven of the 10 most expensive U.S. cities are located, one in five buyers already spends more than half of pretax household income on housing -- much more than the 30% recommended by the Housing & Urban Development Dept."

"Despite the lenders' precautions, some borrowers will receive a rude shock starting this year. Repayment terms on about $1.3 trillion of adjustable-rate loans will increase in 2006 and 2007, forcing some borrowers to pay up to 150% more per month. "In the hands of an unsophisticated borrower, [these loans are] dangerous," says Robert W. Visini, vice-president for marketing at San Francisco mortgage tracker LoanPerformance (FAF).

"About 10% of U.S. households now face a great risk of running into credit problems, according to research done by Meredith Whitney, senior financial institutions analyst for CIBC World Markets Inc. (BCM ). If borrowers start to default on their loans, their lenders could themselves face mounting problems."

"Real estate rates at highest level in nearly 4 years," according to Frank Nothaft, Freddie Mac, as reported by Inman News.

"Mortgage rates this week climbed for the fourth straight week to highs not seen since the summer of 2002, according to surveys conducted by Freddie Mac and Bankrate.com."

"Mortgage rates this week climbed for the fourth straight week to highs not seen since the summer of 2002, according to surveys conducted by Freddie Mac and Bankrate.com.""In Freddie Mac's survey, the 30-year fixed-rate mortgage rose to an average 6.53 percent for the week ended today, with an average 0.6 point, up from last week's average of 6.49 percent. The 30-year fixed has not been higher since the week ending July 12, 2002, when it averaged 6.54 percent.

Foreclosures Soar 63 Percent over Last Year

RISMEDIA, April 19, 2006—RealtyTrac(TM) (www.realtytrac.com), the leading online marketplace for foreclosure properties, today released its March 2006 U.S. Foreclosure Market Report, which shows 101,597 properties nationwide entered some stage of foreclosure in March, a 13 percent decrease from the previous month but a 63 percent increase from March 2005.

Labels: Bay Area Real Estate, Foreclosure, Freddie Mac, Housing Market, Mortgage Lenders, Real Estate Cycles, RealtyTrac

Tuesday, April 18, 2006

Sun's Out, Spend Some Time Out Doors!

Take a tip from my two friends, Norm and Andy. Take a breather, spend a little time out doors soaking it all up. What better place than to spend the afternoon strolling the Berkeley Rose garden.

Check out Andy's article at www.myeastbayagent.com, written Thursday April 13, 2006.

And here's what Alhambra Valley looks like in the Spring.

Labels: Bay Area Real Estate, Berkeley Hills, Berkeley Rose Garden, Housing Market, My East Bay Agent, MyEastBayAgent

![]()

Links

Links

{kind=link}